If you’ve been house hunting lately, you’ve probably noticed how challenging affordability still is. That’s exactly why more buyers are starting to consider adjustable-rate mortgages, or ARMs.

Here’s a quick breakdown of how they work and whether they might be a good fit for you.

Why Adjustable-Rate Mortgages Are Getting More Attention

Since a lot of people aren’t too familiar with this type of loan, let’s start with a simple definition. Here’s how Business Insider breaks down the key difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

Basically, one stays pretty consistent throughout the life of your loan.

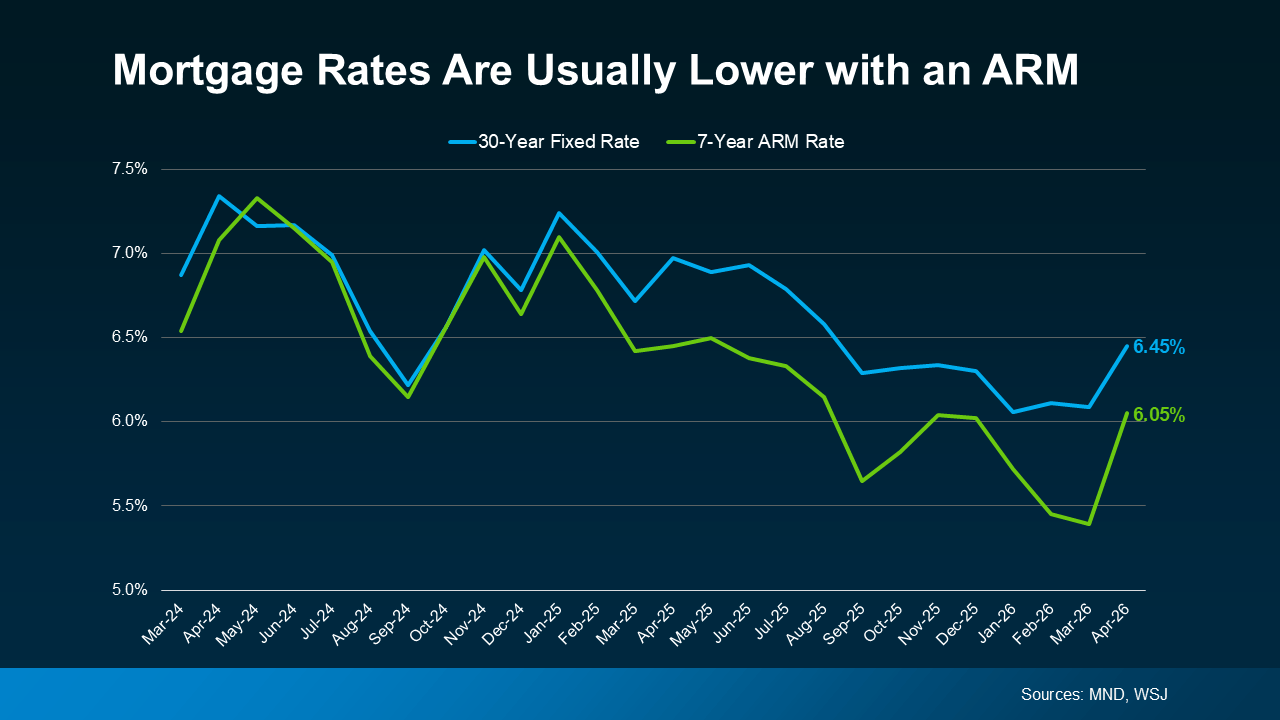

And right now, according to Mortgage News Daily and The Wall Street Journal, the initial rate on an ARM is actually lower than a 30-year fixed mortgage (see graph below):

If you’re curious what that looks like in real dollars, here’s what Redfin found. Based on their research, the typical buyer could save around $150 a month by choosing an ARM over a 30-year fixed mortgage.

For some buyers, that monthly savings can really make a difference.

More Buyers Are Choosing Adjustable-Rate Mortgages Today

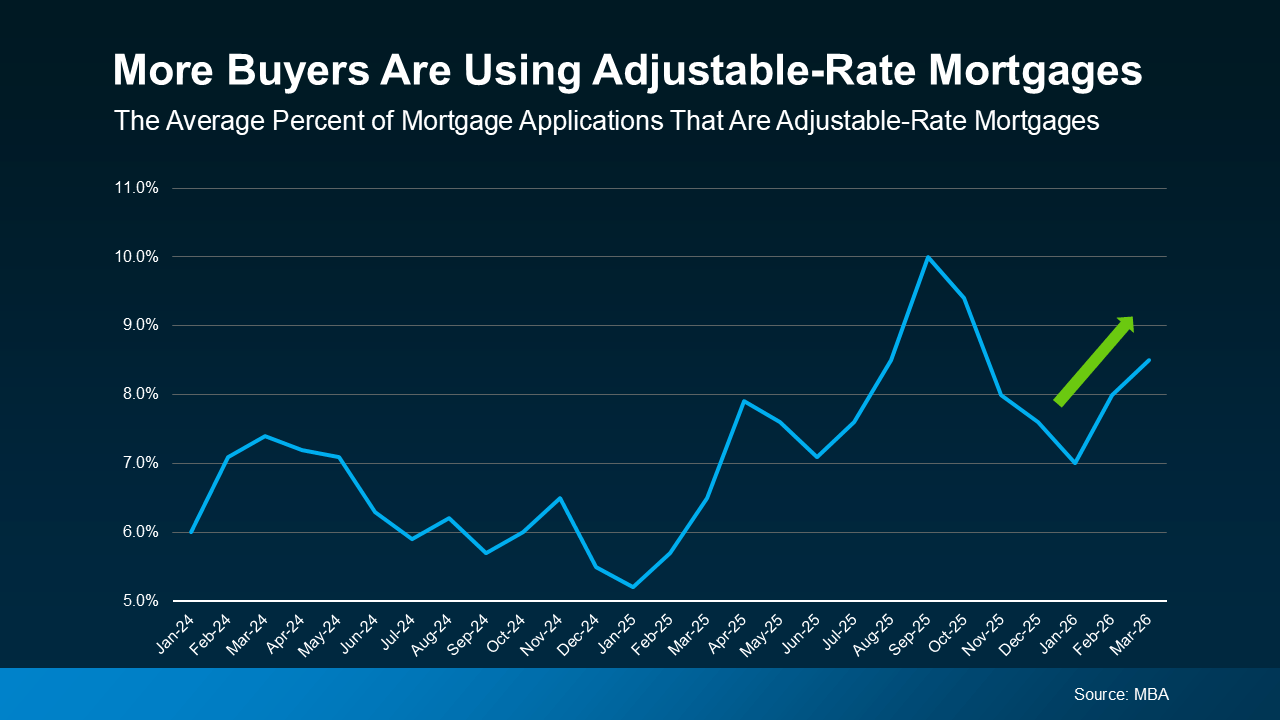

More and more buyers are deciding they’re okay with a little uncertainty down the road if it means a lower payment right now. Data from the Mortgage Bankers Association (MBA) shows that the share of buyers choosing ARMs has been on the rise, especially over the past few years (see graph below).

That doesn’t mean ARMs are becoming the go-to choice for everyone. It just means some buyers are choosing this option so they can still make a move and buy today.

And if you remember the housing crash, it’s totally normal to feel a little concerned seeing ARMs become more popular again. But here’s the good news—today’s ARMs aren’t the same as they were back then.

Back then, some buyers ended up with loans they couldn’t afford once the rates adjusted. Today, lending standards are much stricter, and lenders make sure borrowers can still handle the payment even if rates go up. So, the comeback of ARMs isn’t a sign of another big crash—it’s really just a reflection of how some buyers are adjusting to today’s affordability challenges.

The Trade-Off – What You Need To Consider

If you’re thinking about an adjustable-rate mortgage, it really comes down to your situation and how comfortable you are with a bit of risk.

An ARM could make sense if you plan to move before the rate adjusts, or if you expect your income to increase down the line. But like anything, there are trade-offs you’ll want to think through.

For example, once that fixed period ends, your rate can change—and your monthly payment could go up, sometimes by a noticeable amount depending on where rates are at that point.

And remember, there’s no guarantee that mortgage rates will drop in the future, so refinancing later might not always be an option. That’s why it’s important to have a plan, consider your long-term earning potential, and work closely with a trusted lender before deciding on an ARM.

Bottom Line

ARMs are getting more buzz lately because they can make buying a home more affordable upfront. But they’re definitely not the right fit for everyone.

The key is knowing how they work, understanding the risks, and figuring out if they fit your plan. That’s why it’s important to chat with a trusted lender and financial advisor before making any decisions.