A lot of would-be homebuyers aren’t on the sidelines because they don’t want to buy a home. They’re there because they think they can’t. And more often than not, it’s their credit score that’s making them feel stuck.

A Bankrate survey found that about 2 out of every 5 Americans think you need excellent credit to qualify for a mortgage. That belief alone might explain why so many renters say they haven’t bought yet because they think their credit just isn’t good enough.

Maybe you’re feeling the same way. You check your credit score, notice it’s not quite where you want it, and automatically think buying your first place just isn’t in the cards right now.

But here’s the part most people don’t realize.

Even though a lot of people think you need perfect credit to buy a home, that’s not always true.

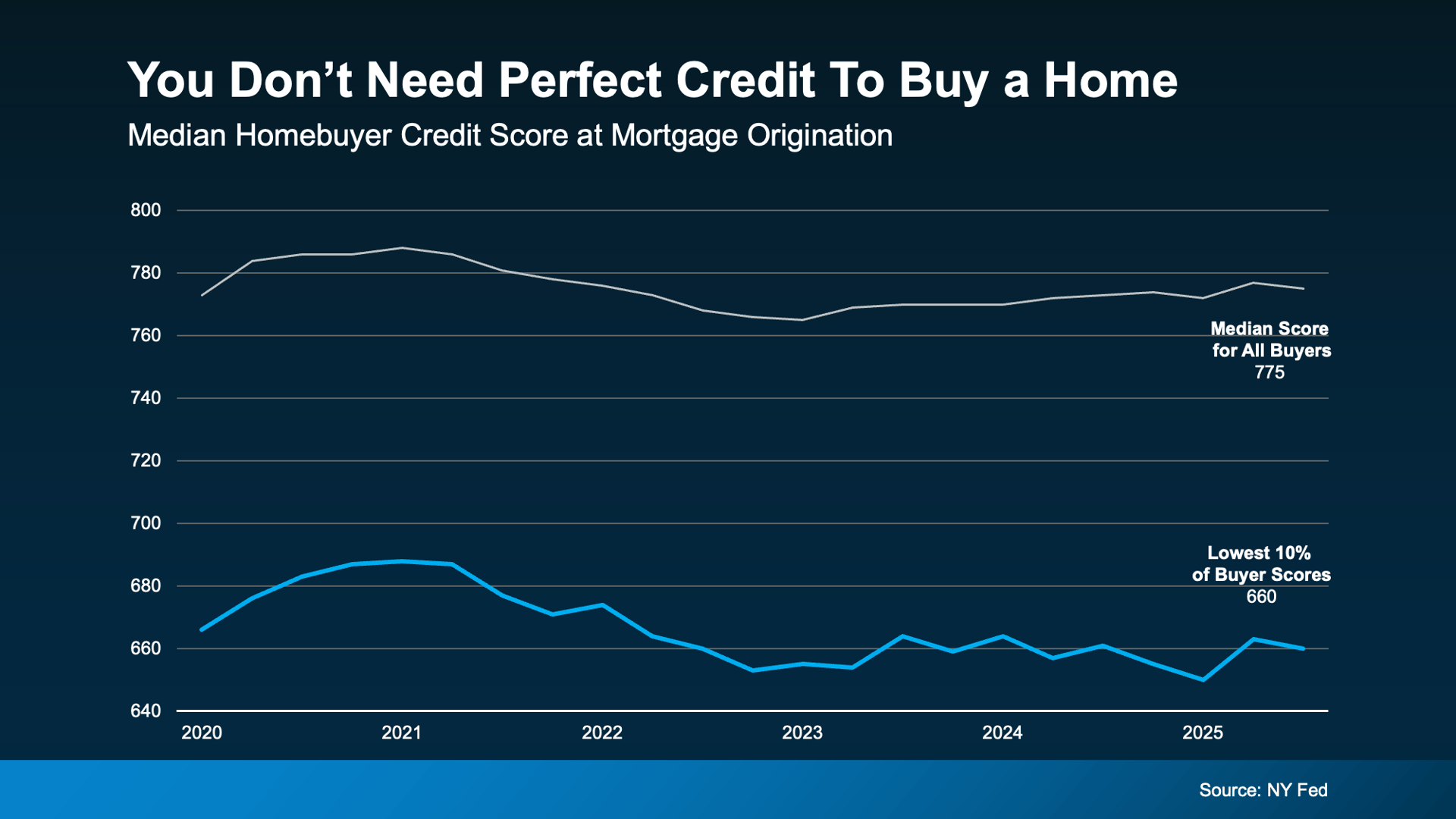

You Don’t Need Perfect Credit To Buy a Home

So where does this myth even come from? A lot of it has to do with the fact that today’s typical homebuyer does have pretty solid credit. According to the New York Fed, the median credit score for buyers right now is around 775—which can make it seem like that’s the standard you have to meet.

But that doesn’t mean your credit score has to be anywhere near that high to actually qualify.

And when you look at recent homebuyers, plenty of them were able to get a mortgage with credit scores well below that number. In fact, data shows that about 10% of buyers had scores around 660. Some were higher, some were lower—but that range shows you definitely don’t need perfect credit to get approved (see graph below).

So even if your credit score isn’t where you’d like it to be, that doesn’t automatically mean the door is closed. FICO even points out that there’s no single credit score you must have to buy a home.

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

Your best next step is simply to talk with a trusted lender and explore what’s possible for you. With plenty of buyers getting approved with credit scores in the 600s, you might be closer to homeownership than you think.

Bottom Line

Your credit score definitely matters—but it doesn’t have to be perfect.

If your credit score is the main reason you’ve been putting off buying a home, it might be worth taking another look at what’s actually possible. And if you want help figuring out where you stand and what your next step could be, a quick chat with a local lender can really help.

You don’t have to have it all figured out before starting the conversation.