The Fed is meeting this week, and a lot of people expect them to cut the Federal Funds Rate. But here’s the big question—does that automatically mean mortgage rates will fall too? Let’s break it down.

The Fed Doesn’t Directly Set Mortgage Rates

Everyone’s watching the Fed right now. Many economists think they’ll cut the Federal Funds Rate at their mid-September meeting in an effort to keep a possible recession from taking hold.

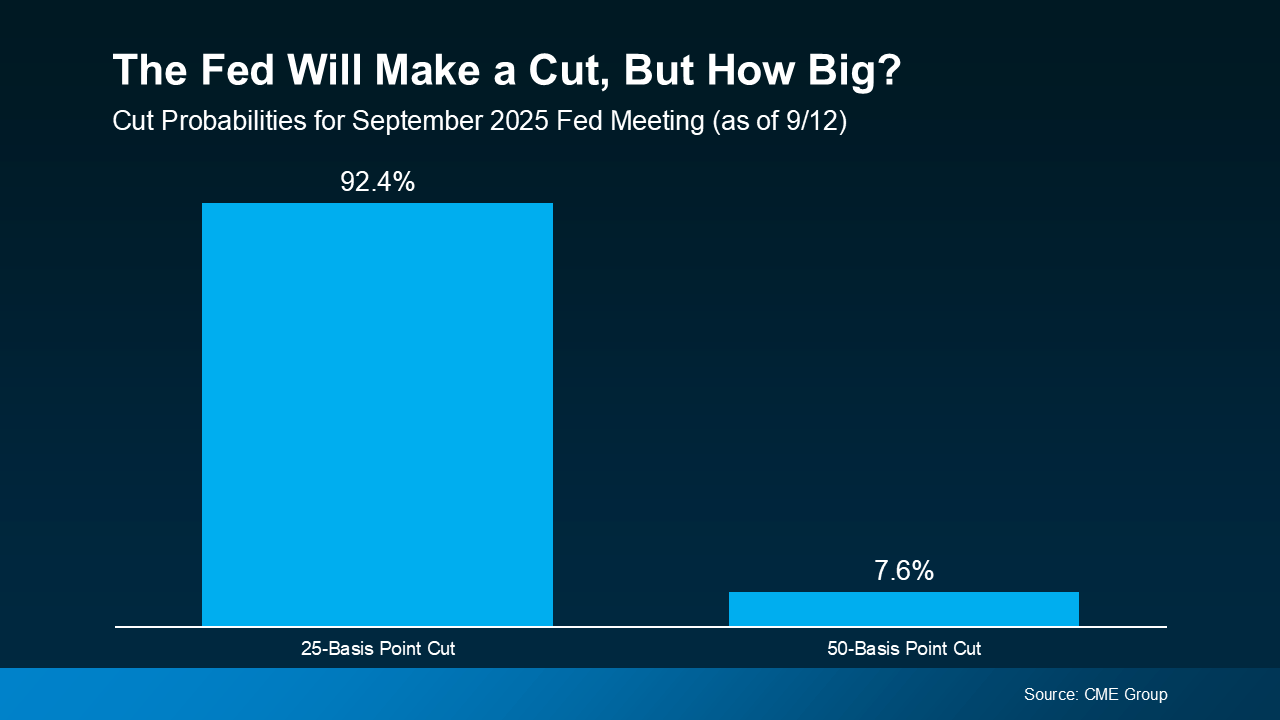

The CME FedWatch Tool shows the markets are basically all in on a September rate cut. Right now, there’s almost a 100% chance it happens. The odds suggest about a 92% chance it’ll be a smaller cut (25 basis points) and only an 8% chance it could be a bigger one (50 basis points).

So, what’s the Federal Funds Rate, anyway? It’s basically the short-term interest rate banks charge each other. While it influences borrowing costs throughout the economy, it’s not the same as mortgage rates. That said, the Fed’s moves can definitely nudge mortgage rates one way or the other.

Why Markets Already Saw This Cut Coming

Here’s something that might surprise you—mortgage rates usually move based on what the markets expect the Fed to do, not just on the Fed’s actual decision. In other words, if markets are predicting a rate cut, mortgage rates often adjust before the Fed even makes it official.

That’s exactly what we saw after the weaker-than-expected jobs reports on August 1 and September 5. Both times, mortgage rates dipped as markets became more confident a Fed cut was on the horizon. And even though the latest CPI report showed inflation ticked up a bit, most still expect the Fed to go ahead with a cut.

So if the Fed follows through with the expected 25-basis point cut, chances are that’s already priced into today’s mortgage rates—meaning we probably won’t see a big drop.

But if the Fed makes a bigger move and cuts by 50 basis points, we could see mortgage rates dip even further than they already have.

So, Where Do Mortgage Rates Go from Here?

Even if this next cut doesn’t make a huge difference, a lot of experts think the Fed could lower rates more than once before the year wraps up—assuming the economy keeps slowing down (see graph below).

Here’s how Sam Williamson, Senior Economist at First American, puts it:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If we see multiple rate cuts—or even if the markets just think they’re coming—mortgage rates could keep easing in the months ahead. The catch? It all depends on where the economy goes. A surprise jump in inflation or any unexpected shifts could change things fast.

Bottom Line

Mortgage rates probably won’t fall dramatically overnight, and they don’t move in lockstep with the Fed’s decisions. But if the Fed starts a rate-cutting cycle—and markets keep expecting more cuts—rates could gradually trend lower through the rest of this year and into 2026.

If you’ve been keeping an eye on the housing market, now’s a great time to talk strategy. Even a small shift in rates can have a big impact on what’s affordable, and knowing what’s ahead can help you make the smartest move for your situation.