If you’ve been out there house hunting lately, you’ve probably noticed how tough those mortgage rates can feel. With rates up and home prices climbing, a lot of buyers are starting to look into different loan options to help make things more affordable. One option that’s getting more attention? Adjustable-rate mortgages, or ARMs.

If you remember the 2008 housing crash, hearing “ARM” might raise a red flag—and that’s totally understandable. But don’t worry, today’s adjustable-rate mortgages are a lot different than they used to be. Here’s what’s changed.

Back in the day, some buyers ended up with loans they really couldn’t afford once the rates went up. But things have changed—lenders are much more careful now. They make sure you’d still be able to handle the payments even if your rate adjusts. So, the comeback of ARMs doesn’t mean we’re heading for another crash. It just means buyers are exploring smart, flexible options to make things work in today’s market.

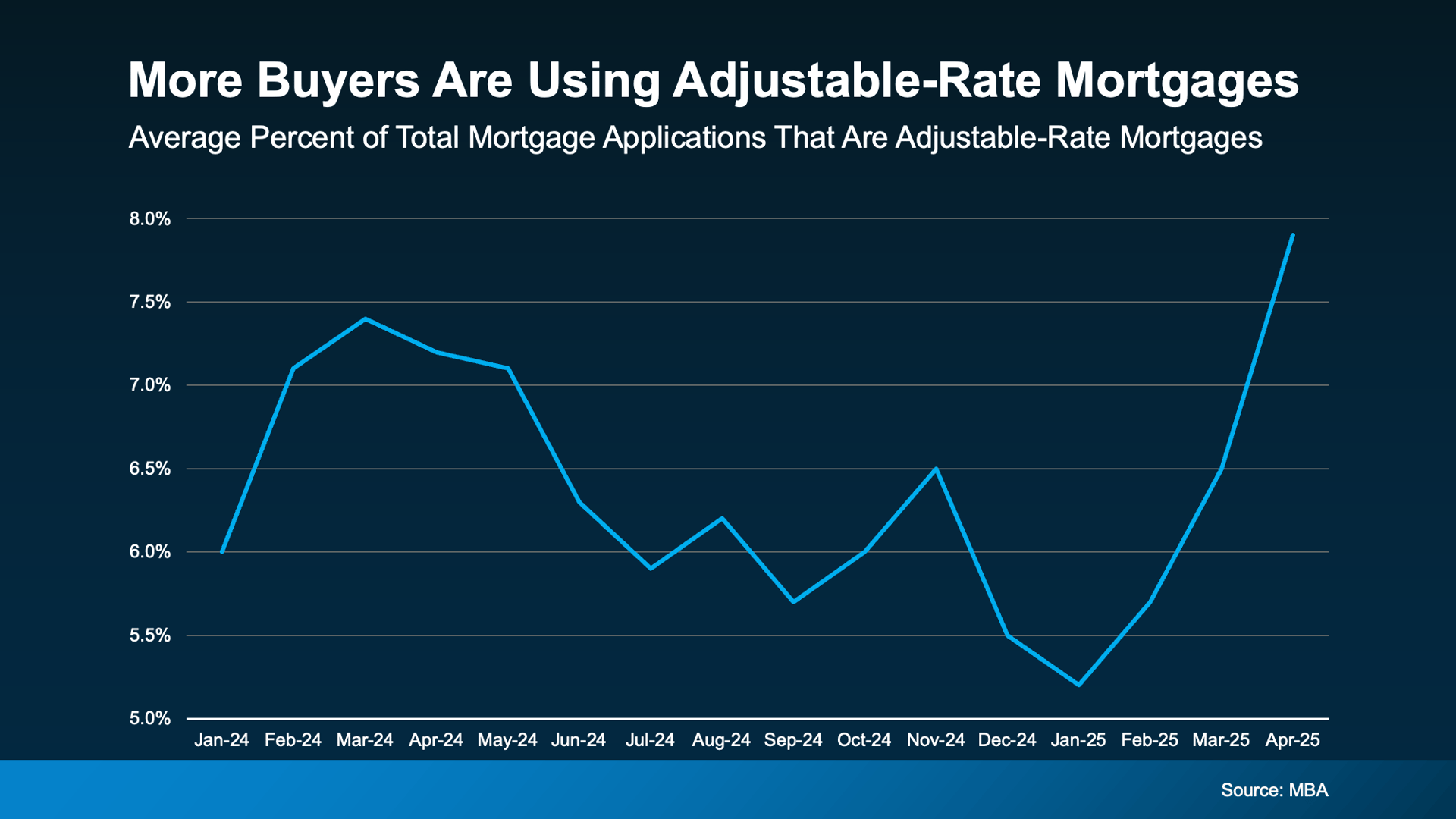

You can see this trend showing up in the latest numbers from the Mortgage Bankers Association (MBA). More and more buyers are choosing ARMs these days—just take a look at the graph below:

ARMs aren’t the perfect fit for everyone, but in the right situation, they can actually offer some great benefits.

How an Adjustable-Rate Mortgage Works

Here’s how Business Insider breaks down the key difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You'll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they've gone down, your payment will decrease.”

Sure, things like property taxes or homeowner’s insurance can still affect your monthly payment on a fixed-rate loan—but the main part of your mortgage stays pretty steady. With an adjustable-rate mortgage, it works a bit differently.

Pros and Cons of an ARM

Here’s a bit more on why some buyers are taking a fresh look at ARMs—they come with some pretty tempting perks, like a lower starting interest rate. As Business Insider puts it:

"Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan."

On the flip side, keep in mind that with an ARM, your interest rate isn’t locked in forever—it’ll adjust over time. As Barron’s points out, that means there’s a chance your costs could go up down the road:

"Adjustable-rate loans offer a lower initial rate, but recalculate after a period. That is a plus for borrowers if rates come down in the future, or if a borrower sells before the fixed period ends, but can lead to higher costs if they hold on to their home and rates go up."

So, those upfront savings can definitely be a big help right now, but it’s important to think about what might happen if you’re still in the house when that initial rate period ends. While projections suggest rates might come down a bit over the next year or two, there’s no sure thing when it comes to forecasts.

That’s why it’s really important to have a chat with your lender and financial advisor. They can help you weigh all your options and figure out if an ARM fits with your financial goals and how comfortable you are with some risk.

Bottom Line

For the right buyer, ARMs can come with some pretty big benefits. But they definitely aren’t a one-size-fits-all kind of deal. The key is really understanding how they work, weighing the pros and cons, and figuring out if they make sense for your financial situation. That’s why it’s so important to talk things through with a trusted lender and financial advisor before making any decisions.