If you’ve got a 3% mortgage rate, it’s understandable that you’re pretty reluctant to let it go. Even if you’ve thought about moving, there’s probably that little voice in your head saying, “Why would I give that up?”

But when you focus too much on that question, you might be putting your own needs on the back burner without even realizing it. Most people don’t move just because of their mortgage rate — they move because they want or need to. So, let’s switch things up and ask something different instead:

How likely do you think it is that you’ll still be living in your current home five years from now?

Take a moment to think about your life and what the next few years might look like. Are you planning to grow your family? Maybe your adult kids are getting ready to move out? Is retirement coming up soon? Or maybe your current place is already feeling a little too crowded?

If nothing’s changing and you love where you are, staying put probably makes total sense. But if there’s even a small chance you might move down the road—even if it’s not right away—it’s definitely worth thinking about your timeline.

Even just a year or two can really change how much your next home might cost.

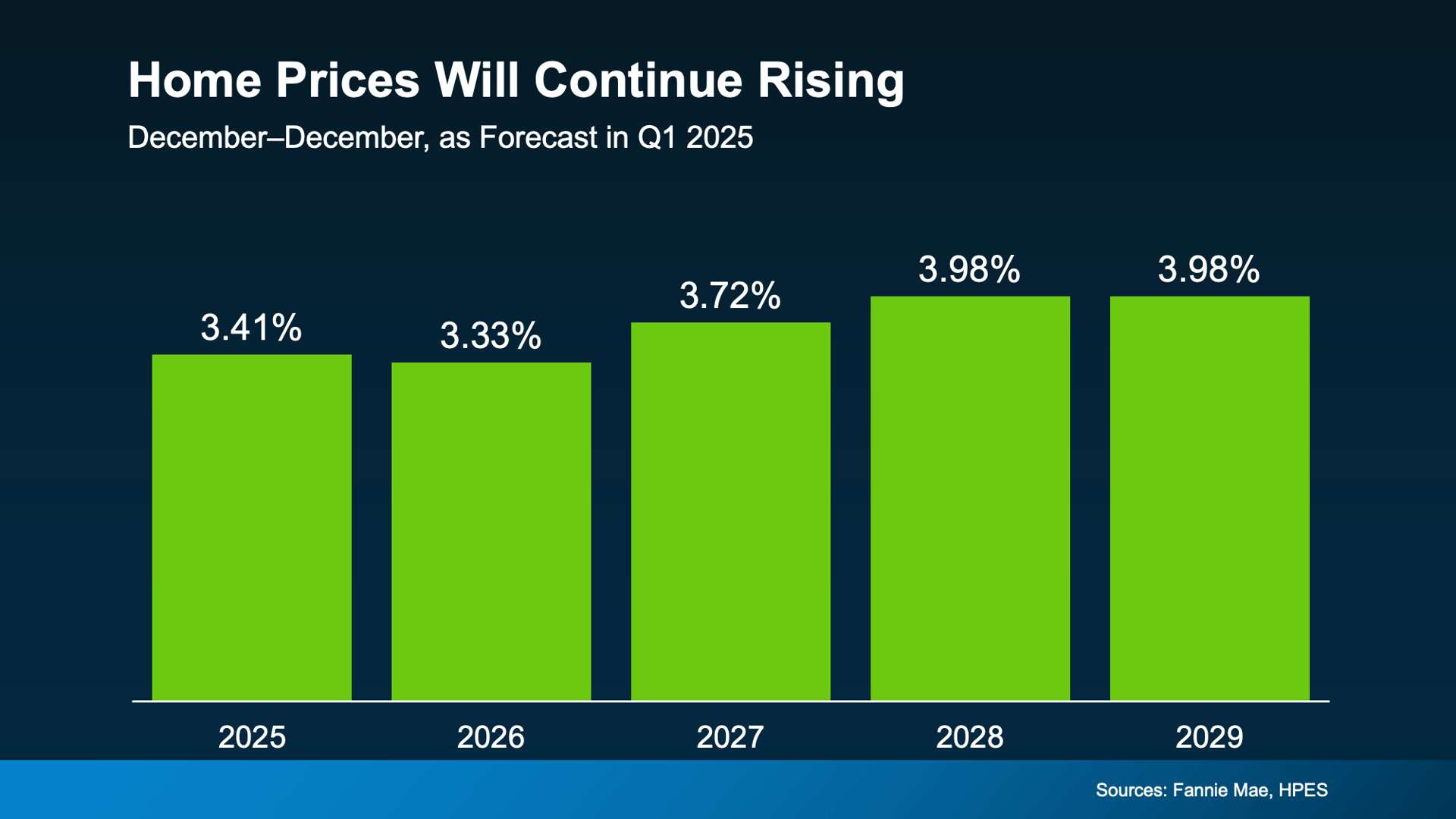

What the Experts Say About Home Prices over the Next 5 Years

Every few months, Fannie Mae checks in with over 100 housing market experts to get their take on where home prices are headed. And the message is pretty clear — prices are expected to keep going up through at least 2029 (check out the graph below):

Sure, those projections don’t show huge jumps every year, but it’s still an increase. Some markets might see prices stay steady, grow slowly, or even dip a bit in the short term. But if you look further ahead, prices almost always go up over time. And over the next five years, even a small increase can add up pretty quickly.

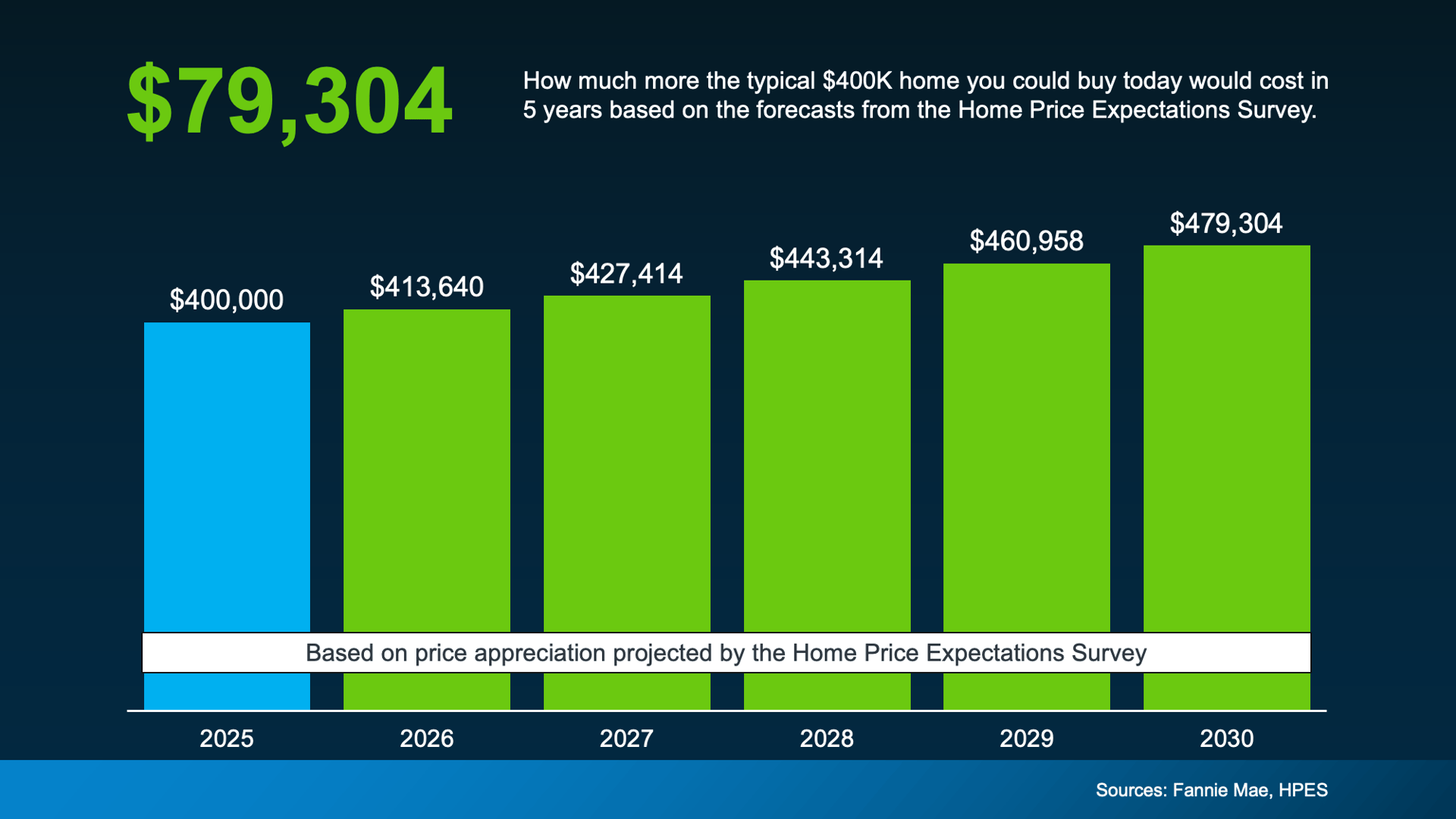

Here’s an example: say you’re planning to buy a house around $400,000 when you move. If you wait and make that move five years from now, these expert projections suggest it could end up costing you almost $80,000 more than it would today (check out the graph below):

Basically, the longer you wait, the more you’re likely to pay for your next home.

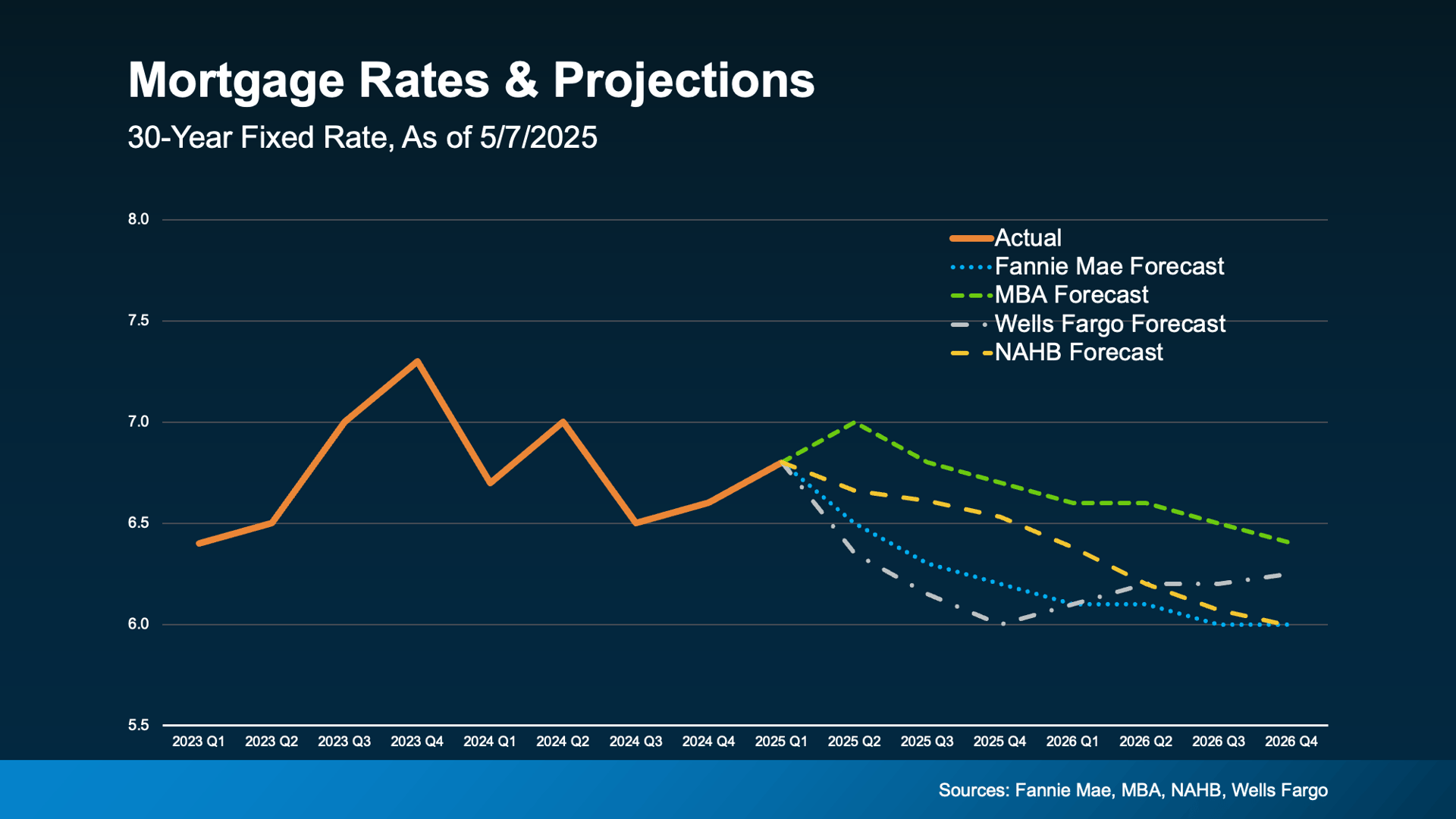

If you’re pretty sure a move is coming eventually, it’s a good idea to really consider your timeline. You don’t have to rush into anything right now, but from a financial standpoint, it could be smart to talk through your options before prices climb even more. While rates might drop a bit, it won’t be by much. And if you’re hoping for those super low 3% rates to come back, experts agree that’s probably not going to happen (check out the graph below):

So really, the question isn’t “Why would I move?” — it’s more like, “When should I?” Because once you look at the real numbers, waiting might not save you as much as you think. And that’s exactly the kind of conversation you want to have with your trusted agent right now.

Bottom Line

Holding onto that low mortgage rate makes sense—until it starts getting in the way of what you really want.

If a move’s probably coming your way—even if it’s a few years off—it’s a good idea to start crunching the numbers now so you can be prepared.

Is there another price range you want to see these numbers for? Let’s chat about it so I can break down how the math works. That way, you’ll have all the info you need to make the best call on your timeline.