With the price of just about everything going up these days, it's no surprise that people are starting to wonder how that might affect the housing market. Some are even asking if we’ll see more homeowners falling behind on their mortgage payments, possibly leading to a spike in foreclosures. And yes, there have been some headlines about an uptick in foreclosure filings—that kind of news can definitely raise concerns. But before you get too worried, let’s put things in perspective.

When you really look at the latest data in context, it’s clear this isn’t anything like the last housing crash—we’re not headed down that same road.

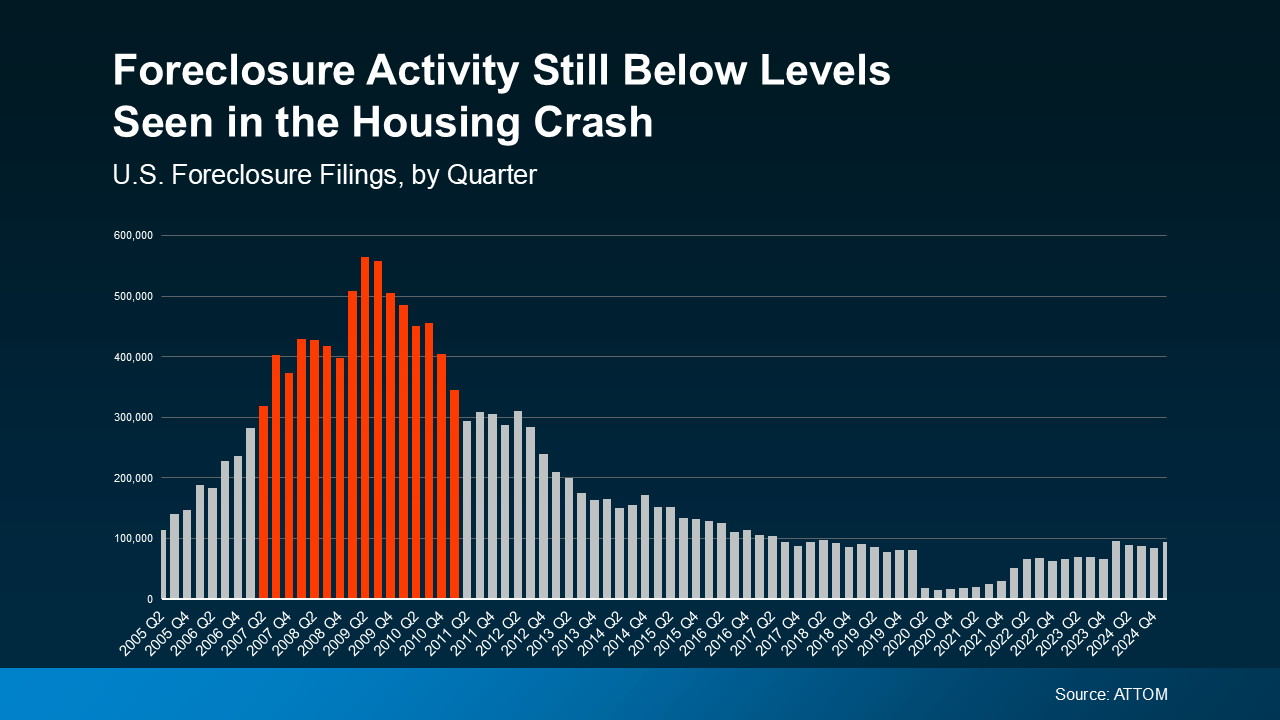

This Isn’t Like 2008

It’s true—foreclosure filings did rise a bit in ATTOM’s latest quarterly report. But even with that bump, they’re still below what’s considered normal, and nowhere near the levels we saw during the housing crash. Seeing it on a graph really helps put it all in perspective.

When you look at Q1 2025 on the right side of the graph and compare it to the years around the 2008 crash (highlighted in red), it’s obvious we’re in a totally different place now. Just take a look at the graph below—it really tells the story.

Back in the day, risky lending practices put homeowners into mortgages they just couldn’t handle. That ended up causing a surge in foreclosures, flooding the market with distressed properties, and creating a huge surplus of homes. As a result, home prices took a big dive.

These days, lending standards are a lot stricter, and most homeowners are in a much better financial spot. That’s why foreclosure filings are so much lower now.

So, don’t compare today to that low point from a few years ago. If you look at more normal years, like 2017-2019, you’ll see that foreclosure filings are actually lower than usual—and a lot lower than the levels we saw during the crash.

Of course, no one wants to go through foreclosure, and it’s definitely emotional because real lives are affected—that’s something we can’t ignore. But overall, this increase isn’t a sign that the market is in trouble.

Why We Haven’t Seen a Big Surge in Foreclosures

Here’s another reason to feel reassured: homeowner equity. In the past few years, home prices have gone up a lot, which means today’s homeowners have built up a strong financial cushion. As Rob Barber, CEO at ATTOM, puts it:

“While levels remain below historical averages, the quarterly growth suggests that some homeowners may be starting to feel the pressure of ongoing economic challenges. However, strong home equity positions in many markets continue to help buffer against a more significant spike . . .”

Basically, if someone hits a rough patch and can’t keep up with their mortgage, they might be able to sell their home instead of facing foreclosure. That’s a big difference from 2008, when a lot of people owed more than their homes were worth and had no choice but to just walk away.

Don't overlook the solid equity most homeowners have right now. As Rick Sharga, Founder and CEO of CJ Patrick Company, explains in a recent Forbes article:

“ . . . a significant factor contributing to today’s comparatively low levels of foreclosure activity is that homeowners—including those in foreclosure—possess an unprecedented amount of home equity.”

Bottom Line

Even with the recent rise, foreclosure numbers are nowhere near the levels we saw during the 2008 crash. Plus, most homeowners today are in a much stronger equity position, even with the rising costs.

If you're a homeowner dealing with tough times, reach out to your mortgage provider to see what options you have.