If you’re like most homeowners, you’ve probably had this thought at least once: “I’d love to move… but I really don’t want to lose my 3% rate.” Totally understandable — that rate has been one of your biggest financial wins, and it’s tough to imagine giving it up. But here’s the thing you don’t want to overlook…

A low rate is great, but it can’t fix a home that just doesn’t fit your life anymore. Things change, families grow, priorities shift — and sometimes your home has to change right along with you. And trust me, you’re not the only one feeling that way.

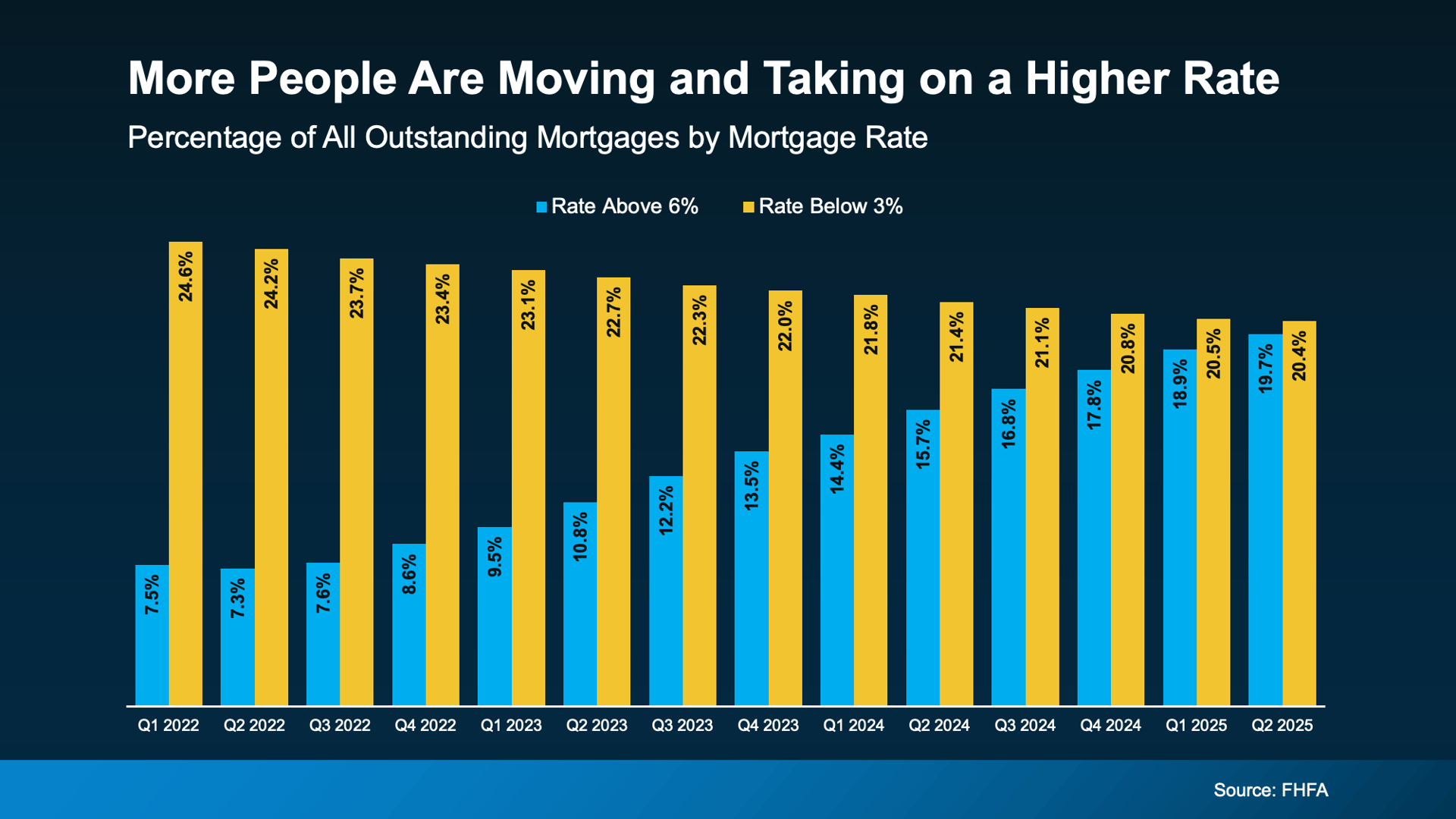

The Lock-In Effect Is Starting To Ease

A lot of homeowners have felt stuck because of something experts call the lock-in effect — basically, not wanting to move if it means taking on a higher rate for your next mortgage. But according to recent data from the Federal Housing Finance Agency, that lock-in effect is slowly starting to ease for some people.

We’re starting to see a shift. The number of homeowners holding onto rates below 3% (the yellow section in the graph) is slowly shrinking as more people decide to make a move. And while some of the folks with rates over 6% are first-time buyers, the group of homeowners with rates above 6% (the blue section) is growing too — because more people are choosing their next home even if it comes with a higher rate.

And even though it might not feel like a huge change, it’s actually pretty significant. The number of mortgages with rates above 6% just reached a 10-year high (see the graph below). That tells us more and more people are starting to accept today’s rates as the new normal.

Why are more people deciding to move these days, even if it means taking on a higher mortgage rate?

It’s pretty simple, really. Sometimes life just can’t wait. Families grow, jobs change, priorities shift, and a home that once felt perfect might not work anymore — no matter how amazing the rate was. And that’s completely okay. As Chen Zhao, Head of Economic Research at Redfin, puts it:

“More homeowners are deciding it’s worth moving even if it means giving up a lower mortgage rate. Life doesn’t standstill—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood. Those needs are starting to outweigh the financial benefit of clinging to a rock-bottom mortgage rate.”

First American calls these key life reasons the “5 Ds.”

-

Diplomas: Getting that degree often comes with a bigger paycheck, which means more buying power. Maybe you bought your first home when you were younger, and now with your career on the rise, it’s time to move up.

-

Diapers: Your space just isn’t cutting it anymore. A new baby or growing family can make your current home feel cramped.

-

Divorce: Life changes like ending a marriage (or starting a new one) can mean you need a fresh place to call home.

-

Downsizing: Maybe the kids have moved out, and you’re ready to simplify. A smaller home means less upkeep and more freedom.

-

Death: Losing a loved one can shift your priorities. You might realize it’s important to be closer to family — life’s too short to be far from the people who matter most.

Whatever your reason, here’s the thing to keep in mind: Sure, that low rate is awesome. But if you stay put, your life might be on hold — and maybe that’s just not working for you anymore.

According to Realtor.com, almost two out of three potential sellers have been thinking about moving for over a year. That’s a long time to put your plans — and your family’s goals — on hold. So maybe the real question isn’t, “Should I move?”

The real question is more like: “How much longer am I willing to stay in a place that doesn’t really fit my life anymore?”

Rates have already come down from their peak earlier this year, and experts expect them to ease a bit more in 2026. When you combine that with the very real reasons you might need a new home, it could be just the push you need to make a move.

The Takeaway

Life doesn’t pause for the perfect rate — maybe it’s time you don’t either.

With mortgage rates already lower than their peak and expected to dip a bit more in 2026, moving could be more doable than you might think. If you’re curious about what’s possible in today’s market, let’s chat.